4.3 - Emission factor selection method

How to select the emission factors necessary for accounting?

This subsection details what an emission factor is, how to choose or develop them from available information, and gives some examples of database (DB) of emission factors.

As a reminder, emissions from each emission source of the organisation are estimated as follows:

Emission from a source = Activity data x emission factor = result ± uncertainty

Emission factors

The emissions quantification method involves defining emission factors (EFs) that convert an organisation's activity data into tCO2e. These EFs represent the average amount of GHGs emitted per reference unit. They do not measure GHG emissions, but estimate them. They typically take the following form:

EF apricot, pitted, raw = 0.88 kgCO2e/kg (source: Agribalyse®)

By multiplying this EF by the number of kilograms of pitted raw apricots consumed by an organisation, it will obtain the GHG emissions associated with that consumption. EFs are therefore essential to carbon accounting, but must be handled with care.

Indeed, EFs are developed from assumptions and underlying studies. An EF covers a specific temporal, geographical and technical boundary. The emission factors for the French average electricity mix, for example, apply only to France and vary by year. It is therefore always important to choose the EF most appropriate to the situation.

Selection of emission factors

Not all EFs are of equal quality, so they must be carefully chosen to achieve accurate. Generally speaking, the broader the boundary an EF covers, the less precise it is, and vice versa.

Thus, when choosing EFs, the organisation shall:

Choose or develop EFs of the best possible quality, in accordance with the various criteria set out above.

Document and retain all EFs used, including in particular their source, units and theuncertainty associated (all characteristics), related documents (DB documentation, sources used, etc.) and any other information deemed relevant, to ensure these emission factors are traceable and comparable from year to year.

Balance efforts: Seeking or developing a highly precise EF for an emission source is often resource-intensive. It is important to ensure careful selection of EFs for significant emission sources. Focusing on action and reducing significant emissions is the core of Bilan Carbone®.

Data collection matrix

This documentation of emission factors is carried out alongside documentation on the activity data used, notably by recording all this information within the data collection matrix, which allows assigning the corresponding ADs and EFs.

The different types of emission factors

The different scenarios an organisation will encounter when selecting emission factors are detailed below.

EFs from databases

A number of EFs are available in databases (DBs), some of which are listed in the following section.

🔎 The reference database for France is the Base Empreinte® of the French Environment and Energy Management Agency (ADEME, French Public Agency for Ecological Transition).

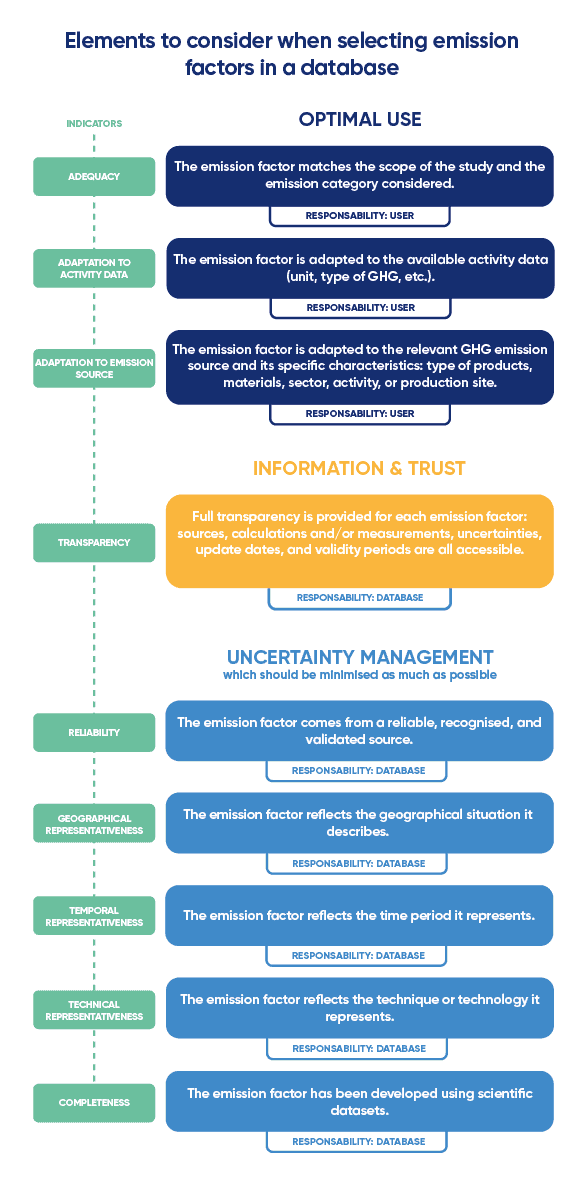

Here are a number of elements to consider, which should be taken into account by the organisation in order to choose the best possible EF from a DB. These selection elements may be the responsibility of the organisation or of the DB (but the organisation is responsible for its choice of DB). When several EFs are available for the same emission source, the organisation shall refer to these elements to arbitrate.

🌐 English version of this image.

{kind=link}

EFs developed by the organisation

If no EF is available for the emission source concerned, or to improve the accuracy or representativeness of an EF, the organisation may:

Approximate this emission source to another emission source that would be similar. This degrades the representativeness of the EF and will result in less precise quantification. The organisation shall therefore use a uncertainty higher than that of the similar EF chosen.

Develop its own emission factor for the emission source concerned.

To develop an emission factor, the organisation shall carry out a relevant life cycle assessment (LCA) and use the "Climate Change" indicator. Note that it is necessary to follow the methodological recommendations for creating EFs of the DB most used by the organisation in order to maintain homogeneity among the EFs used.

Following the LCA, the emission factor will a priori be as representative and precise as possible, because it is specific to the organisation's emission source. Uncertainty arising from the LCA must be associated with the EF obtained.

If this is not possible, the organisation may develop its own EF from, for example, the different raw materials used to create the product (via their respective EFs) or from the carbon accounting of the product manufacturers. In the case of a product that requires machining, manufacturing or assembly phases, the organisation may increase the EFs of the different raw materials by a certain percentage to account for the additional emissions associated with these phases. In all cases, it will be necessary to assign a high uncertainty rate to this EF.

EFs in monetary ratios

Some EFs are expressed as values in kgCO2e/k€ spent, which are notably offered by several DBs. They are called "Spend-based emission factors" or "Non-specific monetary ratios".

While they have the advantage of being usable for data readily available to the organisation (the accounting activity data from the organisation's standard accounting), these EFs have two major disadvantages in carbon accounting:

There are very few of them, and they are derived from averages over many products, and are therefore associated with very high uncertainties. They are also sensitive touse and not always representative of the activity. For example, the monetary ratio "land transport" in kgCO2e/k€ can be used for any land vehicle in the same way, whereas cost is not representative of differences in GHG emissions from one vehicle to another.

They do not allow tracking the impact of actions from one assessment to another. With an assessment calculated from monetary ratios, the only decarbonisation lever becomes reducing the amount of expenditure. However, responsible procurement policies (local, sustainable purchases) are often more costly, which will lead to an increase in the assessment if these purchases are accounted for via monetary-ratio EFs.

An organisation can create its own monetary ratio, for example based on the carbon accounting of its stakeholders. These EFs are called "Specific spend-based emission factors". However, even if the associated uncertainties are low (monetary ratio developed specifically for an emission source), this does not allow fine steering of actions, as the only decarbonisation lever becomes reducing the amount of expenditure.

It is therefore strongly recommended to not resort to EFs "Monetary ratios". These EFs may possibly be used for the following emission sources:

Use of service activities and intellectual services (lawyers, consulting, etc.), but the organisation shall develop "Specific monetary ratio" EFs during its maturity progression.

Non-significant emission sources, for which data are difficult to access (example: small office supplies). The organisation shall nonetheless move away from monetary ratios for these emission sources during its maturity progression.

If the organisation were to use monetary ratios, it may adjust these monetary ratios according to the inflation that applies to its purchases or rental of goods and services.

Requirements relating to the selection of emission factors

Here are different requirements to be met in terms of EF selection for each of the 3 maturity levels.

Beginner level: criterion L1

The share of emissions calculated via emission factors in monetary ratios (specific and non-specific) shall be reported. It is recommended not to calculate more than 30% of the total assessment emissions via monetary ratios.

The use of non-specific monetary ratios must be justified. In the case of non-significant categories or service provisions, the use of these monetary ratios is tolerated by default.

The organisation shall build a robust documentation process that will improve the selection of emission factors for future Bilan Carbone® exercises. If carried out precisely, the data collection matrix can be an integral part of this documentation.

Intermediate level: criterion L2

The use of monetary ratios shall progressively decrease, notably through the calculation of monetary ratios specific to the organisation's partners, contractors or suppliers. The emission factors used shall be refined as the organisation grows in maturity on carbon topics.

The share of emissions calculated via emission factors in monetary ratios (specific and non-specific) shall be reported.

It is recommended not to calculate more than 20% of the total assessment emissions via specific monetary ratios.

The use of non-specific monetary ratios must be justified. Ideally, any non-specific monetary ratio is excluded. It is recommended not to calculate more than 10% of the total assessment emissions via non-specific monetary ratios: any exceedance must be the subject of a detailed justification.

The organisation shall build a robust documentation process that will improve the selection of emission factors for future Bilan Carbone® exercises. If carried out precisely, the data collection matrix can be an integral part of this documentation.

Advanced level: criterion L3

The use of monetary ratios shall continue to decrease, notably through the calculation of monetary ratios specific to the organisation's partners, contractors or suppliers. The emission factors used shall be refined as the organisation grows in maturity on carbon topics.

The share of emissions resulting from a calculation using emission factors in specific and non-specific monetary ratios is reported. It is recommended not to calculate more than 10% of the total assessment emissions via specific ratios and to use no non-specific ratio.

The use of non-specific monetary ratios must be particularly well justified, and in the vast majority of cases excluded.

The organisation shall have developed specific emission factors for key categories.

The organisation shall build a robust documentation process that will improve the selection of emission factors for future Bilan Carbone® exercises. If carried out precisely, the data collection matrix can be an integral part of this documentation.

All information on the operational boundary is documented and Do you have a comprehension question?Consult the FAQ . The method is living and therefore likely to evolve (clarifications, additions): find the.

Last updated