2 - Introduction to the identification of scopes

Introduction to the conduct of step 2: definitions, governance, requirements and deliverables.

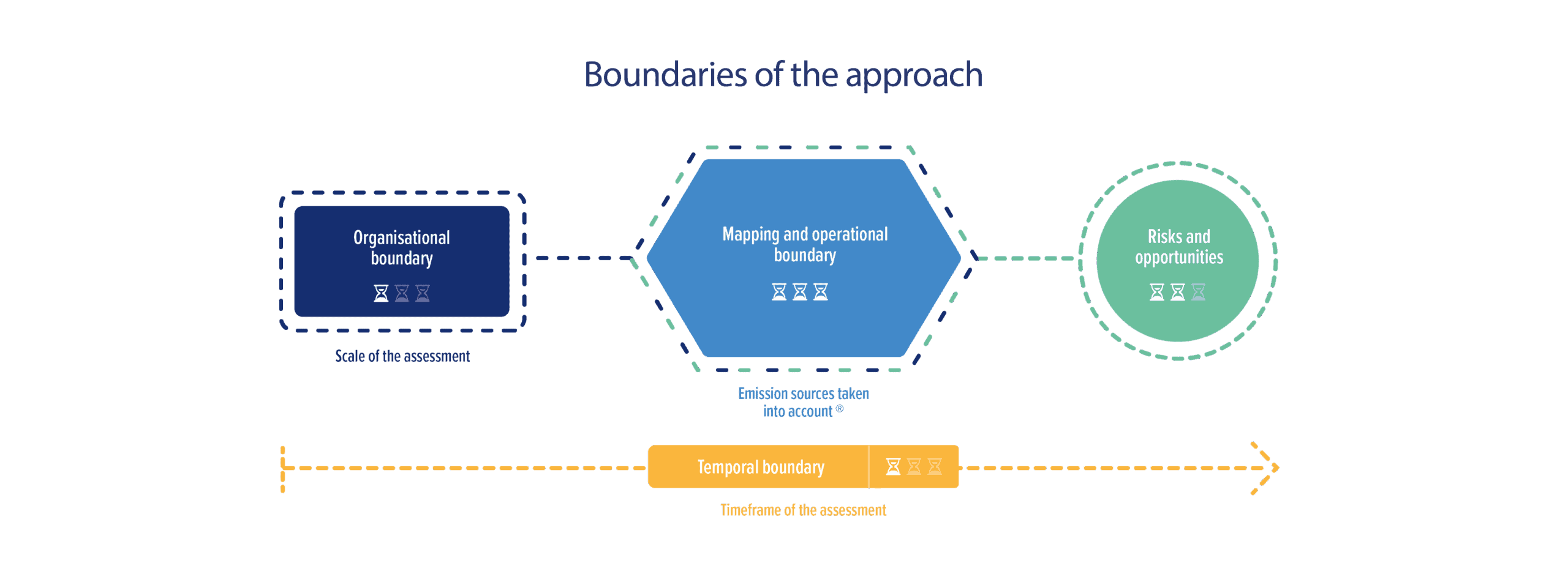

The step of identifying boundaries aims to frame the emissions that will be accounted for. Bilan Carbone® is transparent about the boundaries considered. The organisation shall define:

Step 2.1: the emissions accounted for, which are at minimum the induced emissions (Pillar A).

Step 2.2: the accounting scale: as a reminder this methodological guide applies at the scale of an organisation, so it is about framing the organisational organisational.

Step 2.3: the temporality of the assessment: this is about framing the organisational temporal.

Step 2.4: the identification and mapping of emission sources, allowing the framing of the organisational operational.

Step 2.5: the identification of transition risks and opportunities.

🌐 English version of this image.

{kind=link}

Glossary related to the identification of Boundaries

All terms related to the steps of boundary identification are explained in the glossary. They are reminded below:

Induced, avoided or sequestered emissions: These are respectively the emissions of the organisation (direct or indirect), the emissions of other stakeholders that the organisation enables to reduce, or the emissions that the organisation enables to sequester.

Carbon accounting scale: Four scales mainly: Territory, Individual, Product, Organisation.

Organisational boundary: Set of sites, facilities and equipment taken into account during the organisation's carbon accounting exercise.

Temporal boundary: Specific period of time for the organisation's carbon accounting exercise.

Operational boundary: Set of emission sources taken into account during the organisation's carbon accounting exercise, as well as their breakdown by emission category.

Significance: It is accepted that some indirect GHG emission sources, within an organisation's operational boundary, do not contribute significantly to the total indirect emissions. For an emission to be considered significant, it must meet at least one of the significance criteria. The notion of significance can be useful to set priorities during accounting, when choosing actions or when monitoring results.

Emission source: Physical unit or process releasing greenhouse gases (GHGs) into the atmosphere.

Emission category: Grouping of GHG emissions originating from several homogeneous emission sources. The Bilan Carbone® nomenclature uses the semantics of emission categories. Other standards may use the semantics of scopes or emission categories. Mapping correspondences are possible.

Governance related to the identification of Boundaries

The governance of the boundary identification step is part of the overall governance of the Bilan Carbone® approach presented previously. It is the coordinator who leads the identification of the boundaries.

Requirements related to the identification of Boundaries

As a reminder, here is the summary of the requirements and recommendations, for each maturity level. These criteria are explained in detail in the following sub-sections.

Scope

E: Operational boundary

E1: The assessment shall take into account all direct emissions and between 80% and 100% of the organisation's indirect emissions.

F: Identification of emission sources

F1: The identification of emission sources shall be carried out via a flow mapping.

G: Identification of physical and transition risks

G1: The organisation shall identify the different risks related to climate change (physical risks, transition risks).

Scope

E: Operational boundary

E2: The operational boundary includes all the organisation's direct and indirect emissions.

F: Identification of emission sources

F2: The identification of emission sources shall be carried out via a flow mapping.

G: Identification of physical and transition risks

G2: The organisation shall identify the risks specific to it, and formalise a link with the flow mapping to problematise vulnerabilities.

Scope

E: Operational boundary

E3: The operational boundary includes all the organisation's direct and indirect emissions.

F: Identification of emission sources

F3: The identification of emission sources shall be carried out in a flow mapping or an analytical mapping.

G: Identification of physical and transition risks

G3: The organisation shall carry out or have carried out (from pre-existing or complementary work) a proper analysis of the physical and transition risks that concern it, and quantify the effects that these risks may have on its entire value chain.

Deliverables related to the identification of Boundaries

The information and deliverables obtained at the end of step 2, and associated with the above requirements, are to be reported at the end of the approach:

All information on the operational boundary is documented and Do you have a comprehension question?Consult the FAQ . The method is living and therefore likely to evolve (clarifications, additions): find the.

Last updated