How is the Bilan Carbone® integrated within a low-carbon transition approach?

What is the place of the Bilan Carbone® within a transition pathway?

The low-carbon transition approaches are multiple, with a common objective. Transition pathways adapt to the profile and maturity of each organisation, but also to territories, states, individuals, projects, or products, with various tools, methods and regulations available to them.

The Bilan Carbone® is a comprehensive method that intervenes at several stages in a transition approach, seeking to inform an organisation's strategy. The Bilan Carbone® allows both the counting of carbon, voluntarily or in compliance with regulations, while being resolutely action-oriented.

To position the role and relevance of the Bilan Carbone® within a low-carbon transition approach, the following are presented below:

The place of the Bilan Carbone® within the different scales of carbon accounting or how the Bilan Carbone® integrates at the organisational, territorial, individual, or product scale.

The place of the Bilan Carbone® among current organisational carbon accounting standards, that is a comparison of the Bilan Carbone® with other recognised standards, in order to highlight its specificities and complementarities.

The place of the Bilan Carbone® in regulations or how the Bilan Carbone® meets the legal and regulatory requirements regarding accounting and reporting on carbon.

The place of the Bilan Carbone® in its transition pathway to illustrate how the Bilan Carbone® fits into an organisation's overall low-carbon transition pathway, from emissions analysis to the implementation and continuous improvement of reduction actions within the framework of a genuine transition strategy.

1️⃣ The different scales of carbon accounting

In the context of carbon accounting, four main scales are generally distinguished:

Territories : this scale applies to a specific geographic region, such as a city, region or country. It includes the organisations located there, the individuals living there, and therefore all activities taking place there. Two complementary methods exist: one focuses on GHG emissions produced strictly on the territory (inventory or cadastral approach). The other also accounts for indirect emissions produced outside the territory but necessary for its functioning and the activities taking place there (footprint or responsibility approach). As with organisations, the cadastral approach is concerned with emissions for which the territory is directly a contributor—occurring within it—whereas the footprint approach allows conclusions about the territory's dependence on fossil fuels and its vulnerability to the challenges of the low-carbon transition.

Individuals : this scale focuses on the GHG emissions attributable to a person's activities. A reference method frames the method for estimating an individual's footprint in order to provide exhaustive and educational information on their climate contribution and levers for action.

Products : this scale assesses the GHG emissions associated with a product (good or service) throughout its life cycle, from design to end of life. Several complementary methods focus on the product-specific carbon footprint. ABC notably carries out work with its partners to better integrate product footprint into transition strategies.

Organisations : this scale concerns the GHG emissions induced by all the activities of an organisation, whether it is a company, an association or a public establishment. The activities taken into account by organisational carbon accounting are included within an organisational boundary . Several complementary methods complementary methods focus on organisations' carbon footprints.

The present method focuses on the organisation scale. This is referred to as Bilan Carbone® Organisation.

⏳[WIP] The methodological principles of the Bilan Carbone® Organisation also apply to Product or Territory approaches. They will be the subject of further reflection over the coming years.

All these scales of accounting are relevant, allowing adaptation to the responsibilities, dependencies, and specific levers for action of each of these stakeholders.

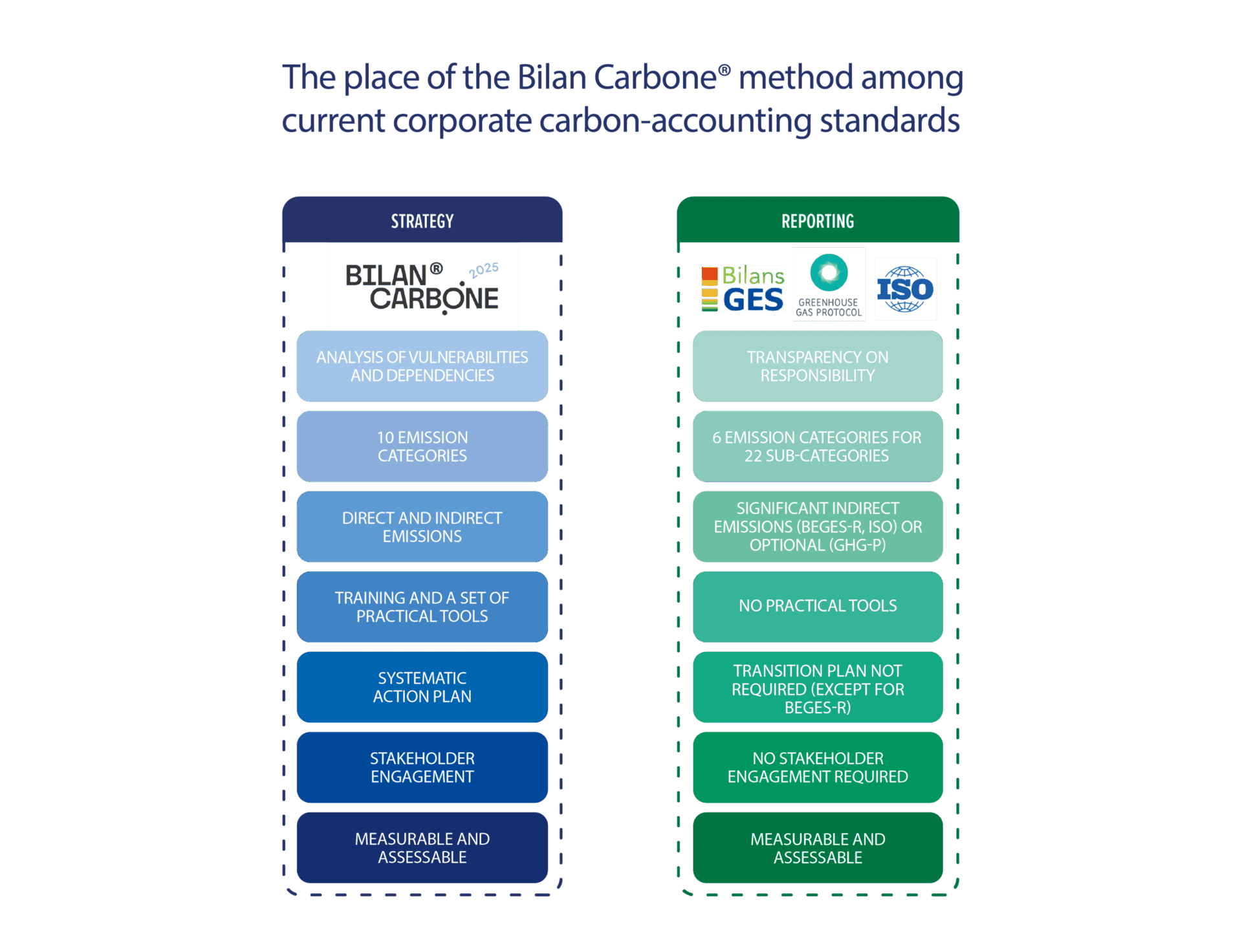

2️⃣ The place of the Bilan Carbone® among current organisational carbon accounting standards

Among the most recognised current standards for organisational carbon accounting, we find:

The French regulatory method for conducting GHG emission assessments (BEGES-R)*

The Greenhouse Gas Protocol (GHG-P)

ISO 14064-1:2006 and ISO 14069:2013 (ISO)

*BEGES-R is a regulation associated with a method, and will therefore also be discussed in the following paragraph concerning regulations.

The Bilan Carbone® and these standards present similarities, complementarities but also specificities.

These standards respond to complementary uses : the GHG-P and ISO standards are generally used for reporting outside France, and BEGES-R for reporting in France. The Bilan Carbone® allows these reportings to be produced, in the formats required by the different standards, but also to produce a strategic analysis of the organisation (notably vulnerabilities and transition opportunities) and to trigger and steer its low-carbon transition.

The Bilan Carbone® method is compatible aligned with the expectations of the GHG-P, of BEGES-R, and of ISO 14064-1. Conversely, following these standards will not systematically meet the Bilan Carbone® requirements: these standards may recommend, without requiring, several essential steps of the Bilan Carbone® (notably on uncertainty management, on accounting for indirect emissions, on Stakeholder engagement or on the relevance of the transition plan).

The deliverables Bilan Carbone® are consistent with the information requested by the other standards. The export of results and the formality of these deliverables may however differ. The Bilan Carbone® results presentation sets out the necessary correspondences allowing the Bilan Carbone® method to be followed and toextract the results in multiple formats. Precautions may however be necessary (for example to work in significance to follow the spirit of ISO or BEGES-R, not to depreciate fixed assets in the case of the GHG-P). The precautions to identify are specified where appropriate.

An important specificity of the Bilan Carbone® lies in its positioning as a comprehensive approach, in which carbon accounting is only one step. Unlike other carbon accounting standards, the Bilan Carbone® method also emphasises Stakeholder engagement and action planning. The method's granular requirements allow the organisation to gain maturity at each repetition of the exercise, in a progressive and long-term approach, until it becomes an environmental management tool.

The boundary to be considered in a Bilan Carbone® also includes emissions on which the organisation is dependent. This makes it possible to act strategically on the organisation's vulnerabilities. It is not a question of determining a responsible party for the emissions, but rather of identifying who can act to reduce them.

Some calculation procedures differ and must be applied with caution:

Emissions associated with energy consumption are calculated with a location-based approach in the Bilan Carbone® and BEGES-R. ISO includes the possibility of doing so also according to a market-based approach. The GHG-P requires calculating both approaches.

Emissions associated with capitalisable goods must be depreciated in the Bilan Carbone® and BEGES-R. The GHG-P requires that these emissions not be depreciated. ISO leaves the choice between the two possibilities.

The emission categories are very similar between these standards, with nonetheless two specificities: ISO includes "GHG removals"; and the GHG-P does not include "visitor travel".

These calculation procedures are set out in the practical guides. It should be noted that it is possible to follow the Bilan Carbone® method, and to export the results according to other standards, by applying these calculation principles.

The table below summarises the similarities and specificities between the Bilan Carbone® and the other current organisational carbon accounting standards:

🌐 English version of this image.

{kind=link}

3️⃣ The place of the Bilan Carbone® with respect to regulations

The Bilan Carbone® seeks to align regulatory obligation and voluntary commitment of all actors in French and European society, so that a voluntary approach can bring benefits with respect to a future obligation, but also that an obliged actor can go further and do more than the regulatory obligation.

The Bilan Carbone® Organisation thus makes it possible to meet, in terms of carbon accounting, two regulations in particular:

The French regulatory method for conducting GHG emission assessments (BEGES-R)*

The Corporate Sustainability Reporting Directive (CSRD)

The French regulation

The Bilan Carbone® method is compatible with the expectations of the regulation:

The Bilan Carbone® at Beginner level meets the regulation on all points.

The Bilan Carbone® at Intermediate level and Advanced level require more.

🔎 Since theevolution of the regulation in France in 2023, there is a very strong correspondence between the philosophies of the Bilan Carbone® and BEGES-R which now also requires an emissions management (complete inventory also covering significant emissions, analytical commentary on the results, renewal of the assessment and comparison of assessments between the base year and the reporting year).

The Bilan Carbone® retains several complementary specificities (approach logic, or strategic analysis logic for example), complemented by the training, tools and community that accompany this method.

The Bilan Carbone® allows carbon accounting on a free boundary and timescale (for example a project, an event, a site). If an organisation subject to regulation wishes to use the Bilan Carbone®, two major precautions must be taken:

The temporal boundary must be a full year of activity (reporting year).

The organisational boundary must be that of the Legal entity subject to the regulation (SIREN).

The CSRD

Following the Bilan Carbone® approach, at its highest level of rigour, allows responding to a large part of the requirements of the ESRS E1 standard of the CSRD, which concerns climate change:

The Bilan Carbone® at Beginner level and Standard do not meet all the requirements of the CSRD (ESRS E1).

The Bilan Carbone® at Advanced level covers the majority of the requirements, listed here.

⏳[WIP] A correspondence table will soon be made available listing the data points (specific pieces of information that the organisation is required to disclose under the CSRD) that a Bilan Carbone® approach at Advanced level will allow to complete.

CSRD declarations require an audit by an independent third-party body. ABC and the National Council of the Order of Chartered Accountants have drafted an evaluation guide for a Bilan Carbone®, a BEGES-R and an exercise specific to the CSRD so that evaluation practices are common and shared, to seek ever more synergies and clarify transition issues for all organisations.

4️⃣ The Bilan Carbone® in a low-carbon transition approach

An organisation encounters several needs throughout its maturity progression on transition issues:

Knowing its context : What are the demands of its stakeholders? What are its regulatory obligations? What are the best practices in its sector? An organisation first needs to motivate its transition action. Several resources are available, notably the sectoral guides from ADEME, but also the content provided by ABC. The Bilan Carbone® proposes here to define several boundaries (organisational, operational, temporal) in order to size the exercise appropriately with regard to the organisation's context. An analysis of transition risks and opportunities is required within the Bilan Carbone® to begin the work of developing a long-term vision of the organisation's low-carbon transition.

Knowing its emissions profile (GHG profile): what are the emission categories? how are they structured? what are the priority(ies) for the organisation in terms of reduction? The international standards but also the French regulation offer methods and reporting formats on this issue, for reporting purposes. The Bilan Carbone® goes further, supporting the organisation from data collection to the production of the GHG profile and its interpretation. Several sectoral versions of the Bilan Carbone® allow organisations in the relevant sectors to focus on sector-specific issues. The Bilan Carbone® also proposes Stakeholder engagement activities to publicise the initial conclusions and encourage action. The Bilan Carbone® offers a voluntary audit process, in order to ensure optimal quality of its results and the actions that follow.

Develop and evaluate a transition strategy : how to define reduction objectives? how to create a transition plan that will allow these objectives to be met? how to integrate this transition plan into the organisation's overall strategy? how to monitor and improve the organisation's carbon accounting approach? Several methods and tools are complementary here to address all these issues: the Science-Based Targets initiative supports large companies in defining objectives that allow adherence to theParis Agreement and the recommendations of the IPCC ; Empreinte Projets is the new version of Quanti GES led by ADEME, aimed at estimating the impact of a project; ACT Step by Step and ACT Evaluation, two sister approaches supported by ADEME in France and internationally, make it possible to create and evaluate a transition strategy consistent with the GHG profile, ambitious and credible across all aspects of the organisation. The Bilan Carbone® links with these approaches so that the organisation can easily use carbon accounting work and the transition plan within these four approaches. The Bilan Carbone® becomes for the most mature organisations the tool for steering the transition trajectory.

Understand the different possible actions in favour of the transition: what is the interest of developing new low-carbon goods and services? how to integrate sequestration into the organisation's strategy? The Bilan Carbone® is based on the principles of the Net Zero Initiative, designing climate action in three forms : reduction of emissions "at home" (what the Bilan Carbone® organisation enables) - Pillar A, reduction of emissions "elsewhere" via new goods & services - Pillar B - and increasing GHG sequestration within natural spaces or via capture and storage technologies - Pillar C. These three forms of carbon accounting are not interchangeable, because an organisation should maximise its action across all three pillars simultaneously. Note that efforts made on Pillars B and C are also valued in the evaluation approaches of transition strategies, notably ACT.

Publicise its commitment to the transition: What should I communicate to highlight my transition action? How can I communicate it and to whom? Many institutions now ask organisations to publish their GHG assessment, whether for investors (such as CDP), the State (regulation BEGES-R), the European Commission (CSRD), their clients who carry out their own GHG assessment or who want to select committed suppliers. While each stakeholder will tend to request different information, the Bilan Carbone® strives to offer a methodological and technical framework synthesising the expectations of each reference so as to facilitate the organisation's reporting.

The transition pathway is non-linear. Each of these approaches feeds the organisation's reflection and allows it to gain maturity. Pathways are multiple, and in a logic of cycle, continuous improvement and renewal, the Bilan Carbone® meets the need for regular steering of emissions and results.

🌐 English version of this image.

⏳[WIP] The ABC's third panorama on the different transition pathways will be updated soon and will detail the different tools and methods available.

Consult the FAQ . The method is living and therefore likely to evolve (clarifications, additions): find thetrack of changes here follow-up of changes here.

Last updated